Insights

The Growth of Passives

How Passive Index Funds and ETFs are making their mark in India

In this article

- The Problem with Active Funds

- India following a global trend towards Passive shift

- Where are we headed now?

- Conclusion

The Problem with Active Funds

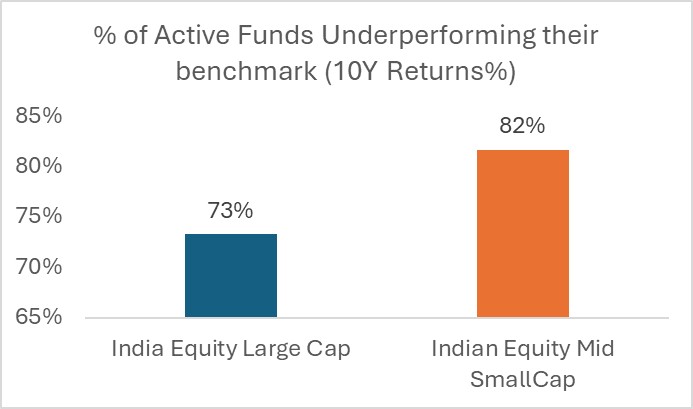

1. 3/4th of Active MFs under-perform the index in the long-term

~73% of large cap funds and 82% of small & midcap funds under-performed the index over a 10-year period. What is surprising is that this underperformance is consistent across fund categories, time horizons as well as asset classes!!

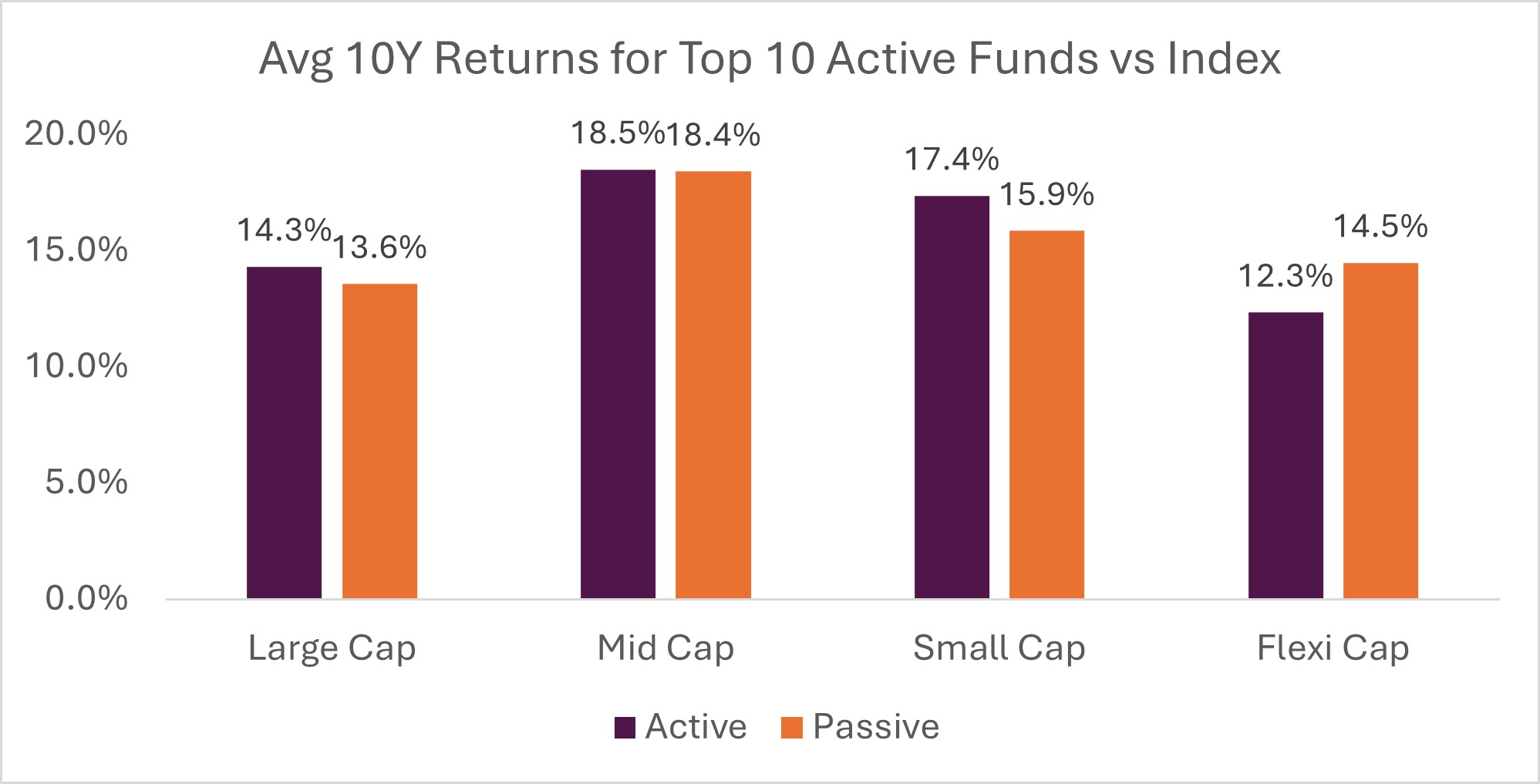

As they say averages can be misleading, so we dug deeper. We looked at “Top 10” Active Funds (by category), and the result was similar. Except for some (~150bps) out-performance in small cap category, active funds have broadly generated returns in line with the index, as can be seen from chart below:

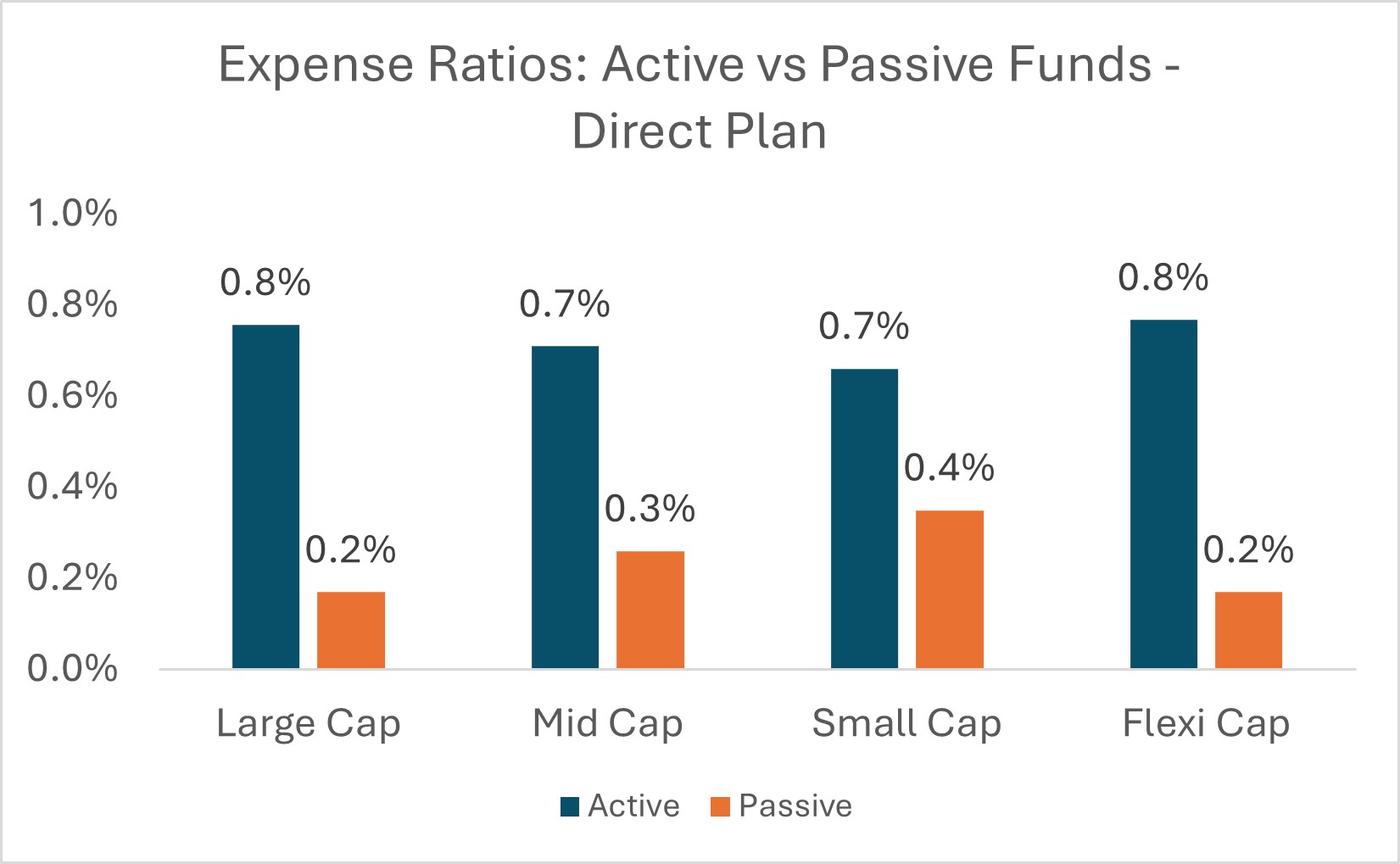

2. High Expense Ratios

Expense ratios of Active funds are as high as 2-4 times that of an average passive fund. Over longer horizons, these expenses weigh heavily on investor returns, for instance – for a 15% return over a 10-year period, the fee difference will turn out to be ~20% of the initial amount invested!

A look at the expense ratios of active and passive schemes shows us clearly that actives are 2-4x more expensive than passives :

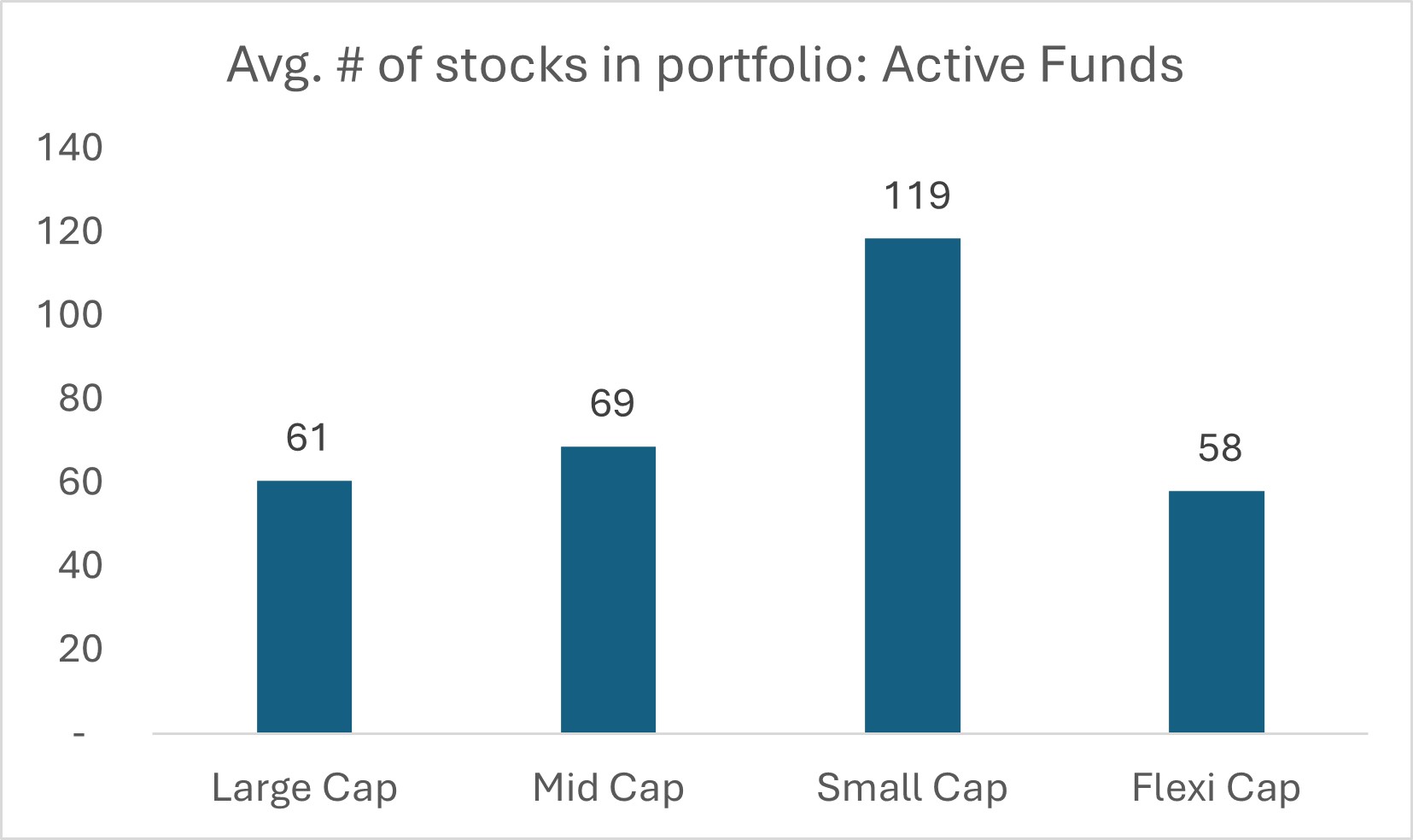

3. Over-diversification:

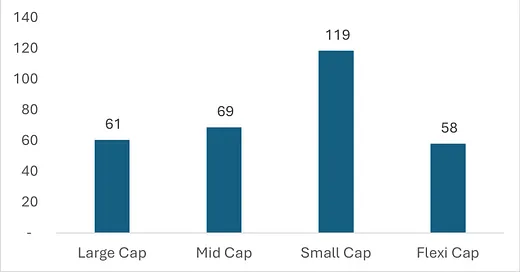

Most funds on an average own ~60 stocks, with Small-Cap funds owning ~120 stocks. Investors who create a portfolio of multiple mutual funds, eventually end up holding as many stocks as the index itself or at times even the entire market of Nifty500. This becomes counterproductive to the goals of active investing.

The chart above shows the average number of stocks held in an average Large, Mid, , SmallCap & Flexi Cap Active Mutual Fund – this is not diversification, but throwing in the kitchen sink!. Though, can’t blame the Fund Managers - they are bound by regulations and blessed with flows, which leads to this over-diversification.

India following a global trend towards Passive shift

Just to get the definition clear → Passive Funds are Index Funds or ETFs (Exchange Traded Funds) which mirror a fixed index and where there is no human intervention with regard to stock selection or portfolio composition.

In today’ age, we prefer less & less human intervention which can be seen in the growth of Driver-less cars, Robotics, Automation, Machine Learning and AI. Financial Markets are no different: the ‘laissez-faire’ (aka Passive) funds are growing faster than the human-managed funds!

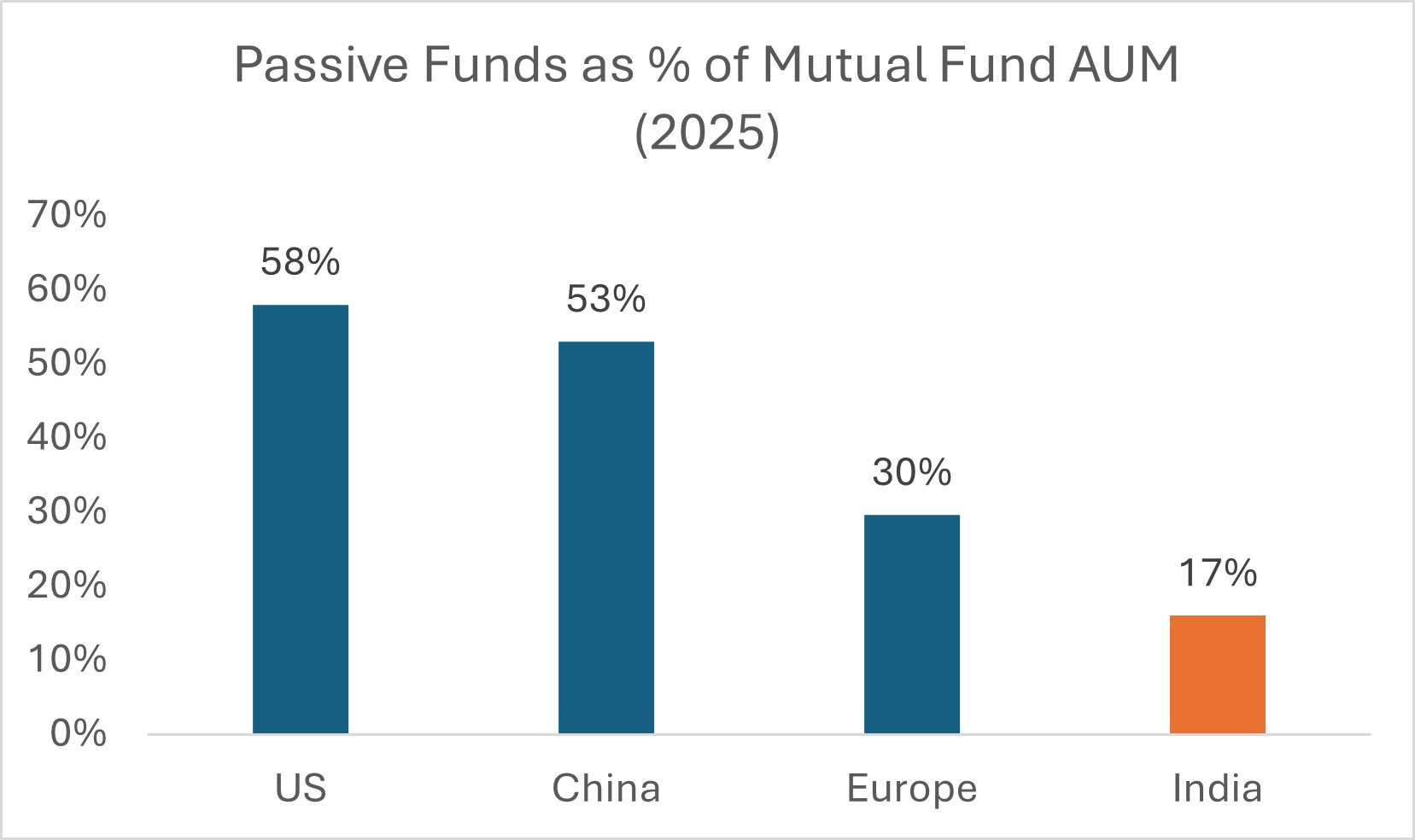

Globally, Passive Funds have picked up in a big way in recent years, especially post Covid. Share of Passives is already trending towards 50%+ in US & China.

The chart below illustrates the share of Passives in MF AUM in the US, China, Europe & India:

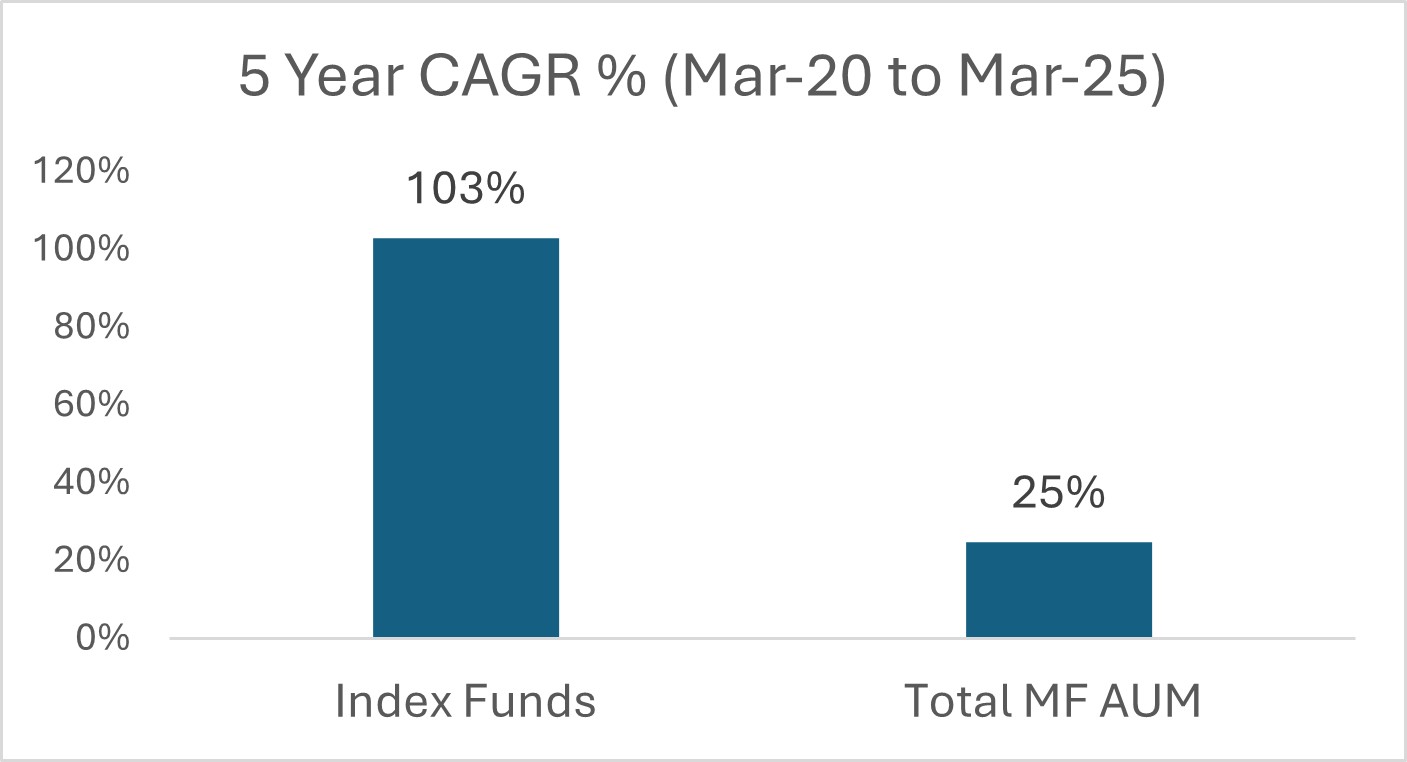

India’s share of passive AUM is lower but it is moving in the right direction: the share has increased from 5% in 2018 to ~17% now in 2025. This is driven by strong growth in passives: FY20-25 AUM CAGR for Index Funds stood at 103% (albeit on a small base) vs 25% for Mutual Funds overall.

Over the last 12months ending June 30th 2025, share of passives in India MF flows is at 24% (For reference: In the US - 85%(!!) of fund flows over the last 12 months were in passives).

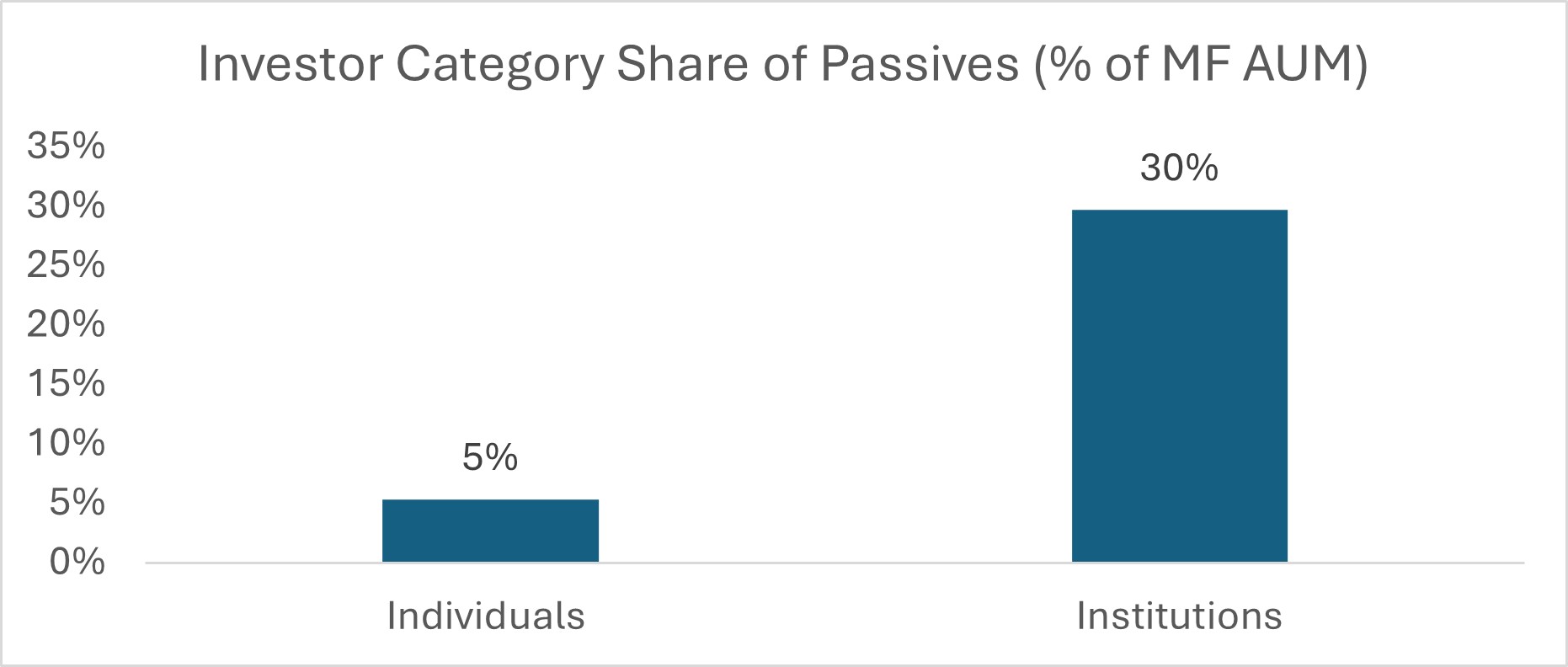

However, while the growth of Passives in India has been encouraging, when we peel the numbers we realize that this is driven largely by Institutions / Corporates. Passive share in Retail + HNI AUM is still only 5% vs ~30% in Institutional AUM. Hence, the growth scope in passives for Retail & HNIs is immense.

Where are we headed now?

We believe that there are structural forces which will further strengthen the shift towards passive funds in India, in line with the global trend:

1. Mean reversion of returns and increased investor awareness:

As is visible in the last 12 months, a combination of time & price correction will bring the market back to mean returns. Post Covid boom has meant that every tom, dick & harry thought of himself or herself as an ace investor. As the tide turns, people will realize that beating the index with active investing is not an easy job on a long term basis. This should lead to increased awareness and a shift towards passive funds.

2. Passive-focused AMCs pushing the right products

Many fund houses are being passive only (like Zerodha) or increasingly focusing on passive funds (like Jio, Navi, etc.). This is visible in the momentum seen in the current year with the introduction of 150 new passive funds — 102 index funds, 3 gold ETFs and 45 other ETFs. (vs 77 in 2024 same period).

3. Smart Beta Funds :

Smart Beta funds primarily invest in “Factors”, which can be style based (such as momentum, quality, value, low volatility) or market-cap based or sector/thematic based. These funds have a higher churn and follow a certain trend, sort of a bridge between active and passive, but at lower costs & taxes. Passive Funds are not just restricted to investing in Nifty50 or Nifty500 companies anymore!

Investments in Smart beta Funds in the US is valued at $2 trillion, and constituted about 16.4% of AUM as of 30th June, 2025.

India is at the inflection point of this shift towards smart beta funds, where a wide array of sectoral, thematic and factor funds will be launched.

Funds like Nifty200 Alpha 30 Index, Nifty Midcap150 Momentum 50 Index, Nifty200 Value 30, Nifty500 Flexi-cap Quality 30 etc. are some of the strategy funds introduced by NSE.

Conclusion

While active funds’ AUM is not expected to degrow, passive funds are witnessing a massive runway of growth ahead of them, potentially reaching a share of 30% of MF AUM over the next 5-7 years (from about 17% currently).

Given the wide varieties of passive funds across market-cap, factors, sectors, etc. along with multiple fund houses offering them - the key will be to choose the right product. Hence, we also foresee that ETF/Index fund baskets could become popular and a new breed of passive-focused advisors could rise.